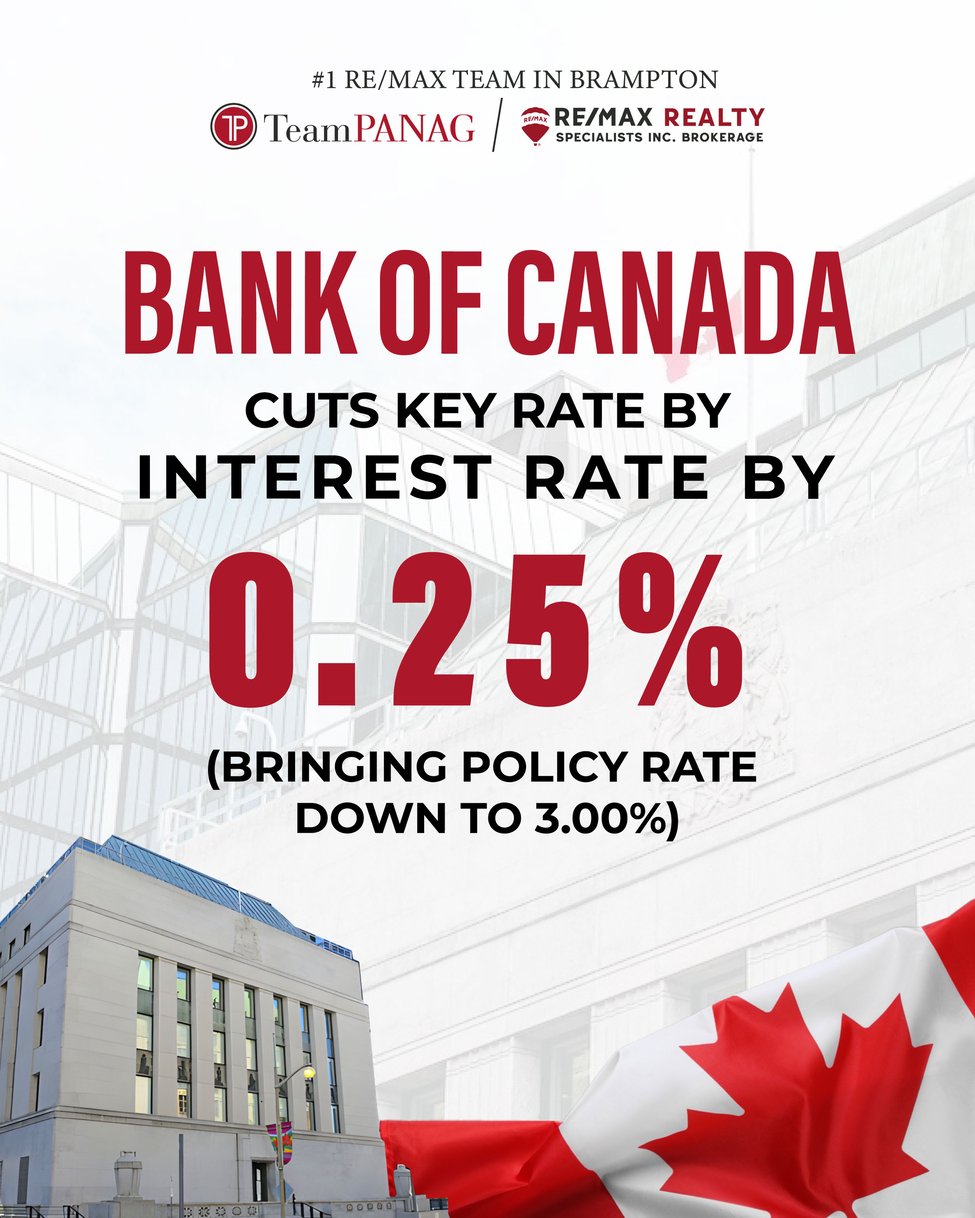

On January 29, 2025, the Bank of Canada made an unexpected but significant move, reducing its key interest rate by 0.25%, bringing it to 3%. This decision marks a pivotal moment in Canada’s economic landscape as it seeks to balance inflation concerns with the broader need to stimulate growth in a period of economic uncertainty.

What Does This Rate Cut Mean?

For Canadians, this means lower borrowing costs, which could impact everything from mortgages to personal loans, and even credit card interest rates. If you’ve been contemplating a new loan or refinancing an existing one, now may be the time to act. Lower interest rates usually encourage borrowing, as consumers can expect to pay less interest over time.

Impact on Mortgages

With the Bank of Canada’s key interest rate lowered, variable-rate mortgage holders will likely see a decrease in their interest payments. Fixed-rate mortgage holders, however, are unlikely to see immediate changes, unless they decide to refinance. If you're thinking about buying a home, this could be a good opportunity to lock in a lower rate before any future hikes.

What About Inflation?

Despite the cut, inflation remains one of the Bank of Canada’s key concerns. The decision to reduce rates, though small, is likely aimed at stimulating the economy without fueling runaway inflation. It reflects the central bank's cautious approach to finding the balance between nurturing growth and keeping price pressures under control.

Stimulating the Economy in Uncertain Times

Canada’s economy has been navigating challenges such as global economic slowdown and fluctuating commodity prices. With the rate cut, the Bank of Canada is attempting to boost consumer spending and business investment, giving a much-needed boost to the overall economy. For businesses, this could make it easier and cheaper to borrow funds for expansion or investment in new projects.

Should Canadians Be Worried?

While the rate cut is aimed at spurring economic growth, it does signal that the Bank of Canada is concerned about the current economic outlook. It could be a sign of softer growth, and the bank may not rule out further cuts if the situation doesn't improve. However, for most consumers, the immediate impact will likely be positive, with lower borrowing costs and better access to credit.

Looking Ahead: What’s Next?

As we move into 2025, it remains to be seen whether this rate cut will be the first in a series or a one-off adjustment. The Bank of Canada will closely monitor inflation and other economic indicators before deciding whether further cuts or hikes are necessary. For Canadians, staying informed and reviewing your financial situation could help you take advantage of the current environment.

If you have any thoughts on the rate cut or how it might impact your finances, drop a comment below. We’d love to hear your perspective!